Loading page content...

Loading page content...

Aimee Joe Fenny

Author

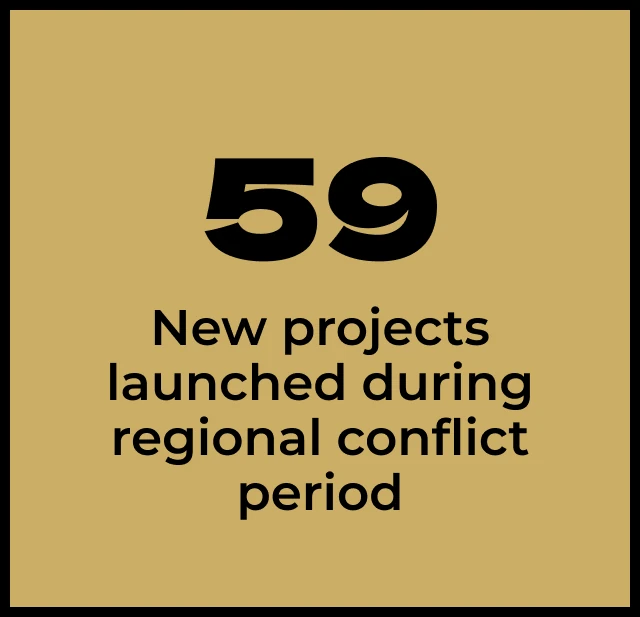

Discover how the UAE real estate market demonstrated exceptional resilience with 59 new property projects worth Dh118.3 billion launched amid regional uncertainty — covering buyer trends, off-plan demand, and expert insights.

In a striking display of structural strength, the UAE real estate sector has launched 59 new residential and mixed-use projects collectively valued at Dh118.3 billion — even as regional geopolitical tensions temporarily shook investor sentiment. Representing over 12,000 units across the Emirates, this wave of activity signals far more than a recovery: it is a decisive affirmation of long-term confidence in the UAE's property landscape.

Regional conflicts have historically triggered sharp pullbacks in emerging real estate markets.

The UAE, however, continues to operate on a different axis. When escalating tensions began affecting Gulf sentiment earlier this year, analysts braced for a slowdown. Instead, the data revealed a market that paused, recalibrated, and resumed with notable momentum.

The sustained launch activity reflected both developer confidence and deep-rooted demand from end-users and investors. According to data from Property Monitor, active users on major platforms rebounded to 85% of the 2026 baseline within 58 days of the onset of the conflict — while unique buyers returned to 87%. Impressions surged to 92% of baseline, a signal that consumer intent remained alive throughout the uncertainty.

Despite market uncertainty, established communities with proven infrastructure and lifestyle credentials continued to attract the strongest buyer intent. For ready apartments, areas such as Jumeirah Village Circle, Business Bay, Downtown Dubai, Dubai Marina, and Arjan dominated search volumes. Villa seekers focused heavily on Damac Hills 2, Dubai Hills Estate, Arabian Ranches 3, Arabian Ranches, and Dubai South — communities known for family-friendly environments and long-term capital appreciation.

In the off-plan segment, Majan, Jumeirah Village Circle, Dubai South, Jumeirah Village Triangle, and Business Bay led apartment interest. On the villa side, marquee master developments such as The Oasis by Emaar, The Valley by Emaar, Damac Lagoons, Dubai South, and Mohammed Bin Rashid City drew strong off-plan commitments. This split between ready and off-plan demand underscores the dual engine powering Dubai's property cycle: end-user occupancy and forward-looking investment.

Rental demand — a leading indicator of real population-driven housing need — remained concentrated in lifestyle-forward and family communities throughout the conflict period. Jumeirah Village Circle, Arjan, Business Bay, Dubai Marina, and Meydan held their positions as the most searched apartment rental destinations. For villa rentals, Damac Hills 2, Dubai South, Mirdif, Arabian Ranches 3, and The Valley by Emaar attracted the highest levels of renter interest.

The persistence of rental demand in these communities reinforces a key market dynamic: the UAE's residential sector is increasingly anchored by genuine housing requirements rather than speculative activity alone.

One of the most significant shifts observed during this recovery phase is the growing sophistication of buyer and renter behavior. Property seekers are increasingly relying on data tools — such as transaction history platforms and automated valuation models — to compare opportunities, benchmark pricing, and validate investment decisions before committing.

This transition toward data-led engagement is not a reaction to uncertainty; rather, it is the market maturing.

High-intent enquiries recovered to 80% of the 2026 baseline, while overall platform engagement metrics collectively demonstrated that serious buyers and qualified agents remained active throughout the geopolitical turbulence. The quality of engagement, not just the volume, has meaningfully improved — a hallmark of a market gaining institutional depth.

For seasoned real estate observers, developer behavior is one of the most reliable sentiment proxies available. Developers absorb market intelligence across research, sales pipelines, and capital availability — and when they choose to launch, it reflects a calculated view that demand exists to absorb supply.

The announcement of 59 projects totaling more than 12,000 units during a period of regional stress carries considerable informational weight.

The total gross sales value of Dh118.3 billion attached to these launches underscores that these are not speculative micro-launches — they represent well-capitalized, diversified offerings designed to meet the expanding appetite of both domestic and international property seekers. The breadth of price points, locations, and product types reflected in these launches further speaks to a market serving a genuine cross-section of demand.

Let our experts guide you through Dubai's luxury property market with personalized advice

Continue exploring insights about Dubai's real estate market